On 15 January 2025, EIOPA published the 5th edition of their annual Consumer Trends Report. This annual publication, along with the Eurobarometer have become a much-anticipated event for the savings industry stakeholders such as employers, pension funds, insurance companies and asset managers. With the wealth of data collected by EIOPA from across the European Union, these reports provide insights into the prevalence of savings products, consumer perceptions of the savings market and the barriers to saving. These insights guide the national pension and insurance regulators towards local actions but also provide the industry with specific guidance on how to tackle challenges to consumer confidence and improve savings rates.

Are we saving in Greece and Cyprus?

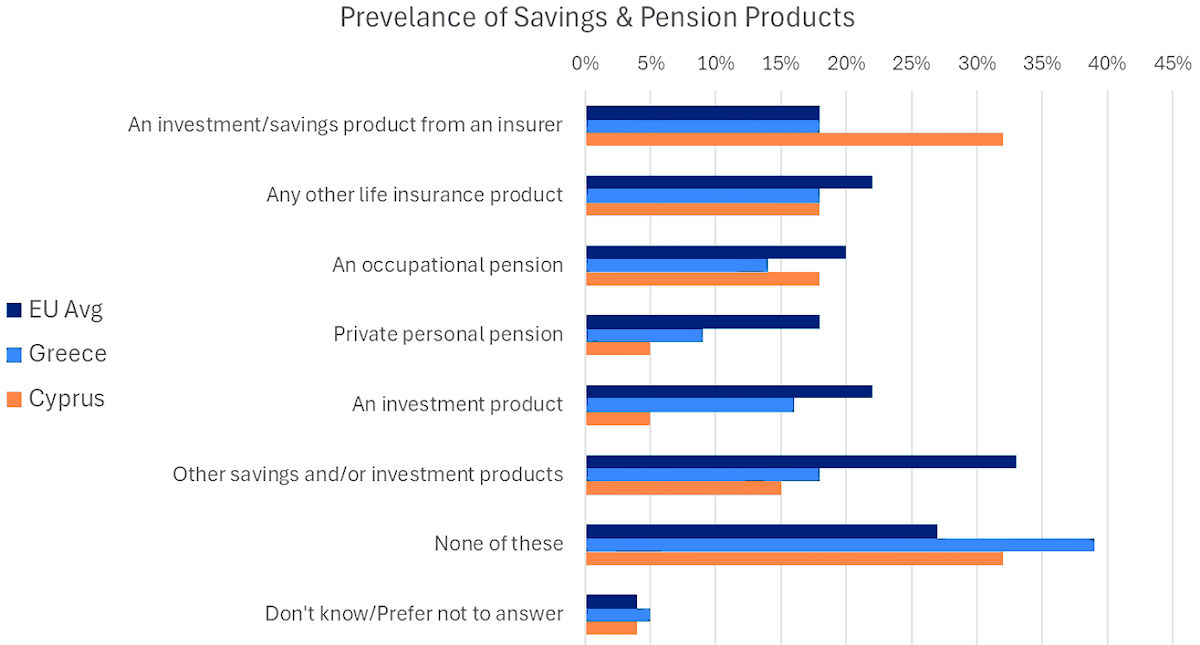

The Eurobarometer 2024 provides detailed statistics on the prevalence of savings and pension products per country.

It is not surprising that different geographies exhibit different prevalence across products given different taxation, social security structures and regulations. However, it is indicative of a systemic problem that in Greece almost 40% and in Cyprus 32% of the population indicated no savings or pension and are clearly relying on social security for old-age pensions, and with no financial recourse for other emergencies. Both are well above the European average of 27% of the population without any savings. This is a strong indicator of financial vulnerability.

A surprising statistic is the general lack of occupational (workplace) pensions, with only 14% of Greeks and 18% of Cypriots benefiting from employer-sponsored plans. This is slightly below, the still disappointing, 20% European average.

An interesting outlier is that 32% of Cypriots reported to owning an investment or savings product from an insurer. This is well above the EU average and Greek population with only 18% ownership.

Are Saving Products a good deal?

One of the central themes of the EIOPA report is the persistent concern surrounding value for money (VfM) in insurance and pension products, which remains a key barrier to savings rates. However, an interesting shift in focus has taken place since the first Consumer Trends Report in 2019. The focus 5 years ago was on transparency of costs, whereas in the 2024 report there is more of a focus on the actual level of charges. Perhaps this illustrates some maturity in transparency following the implementation of the Insurance Distribution Directive and the EU population in understanding or, at least, questioning costs.

However, the focus on costs cannot be overestimated, being the number one factor for consumers to determine the value proposition of an investment product (37% of consumers) followed by good returns (34% of consumers).

Just to illustrate how much of a barrier to saving the VfM perception is, over the last year 17% of Europeans indicated that they did not buy or renew an investment or savings product from an insurer due to the high fees and charges. Cyprus is in line with this European statistic at 16%, but in Greece the result was a very significant 25%.

Life insurers struggle with the perception challenge with less than half of people in the EU considering savings and investment products from insurers to be value for money. The perception from Greeks is better with 54%, and Cypriots exhibit the top result in the EU with 63% confidence, coinciding with the high prevalence of savings through insurance products.

Comparing jurisdictions with different tax systems, broker remuneration structures, insurance products and riders, and mix of new business and existing business, means that the statistics should be interpreted with care.

It may be counter-intuitive that higher commission rates coincide with a better perception of value for money, but could be well explained by:

- Limited access to direct channels in Greece and Cyprus means that highly compensated agents play a crucial role in communicating value to consumers.

- Limited competition and higher charges in the smaller markets may contribute to a skewed perception of value for money. This advantage is likely to erode with the increasing availability of cross-border and online products.

- The lack of readily available market data hinders consumers' ability to compare charges between providers, further limiting competition.

- Prevalence of guarantees and/or other covers within savings products in Greece and Cyprus improves the perception of value with the real cost not easily appreciated by the consumer.

Ironically, from a financial wellbeing perspective, it would be preferable to save regularly through a less efficient product than not save at all due to being overly concerned about costs.

The savings market challenge:

The challenge for European life insurance companies is clear. Either they need to communicate their value to the consumer more effectively to demonstrate they offer a good deal or simply find a way to charge less and closer align with the emerging fintech savings offerings in Europe.

Cost-efficiencies could be realized through:

- Simplified investment strategies; consumers should not pay for complex investment governance models and exotic funds that will deliver marginal or no gains in the long term

- Simplified savings products with limited fund choices and rider benefits

- Digitization, the implementation of which should be well underway for any life insurer with long-term ambitions

- Employing artificial intelligence, a recent development that could assist significantly in accelerating the digitization gains

The European life insurance industry clearly needs to win their clients back in the saving market, but the competition is fierce and growing fiercer.

Don’t forget the pension funds:

Although the value for money paradox is clear for the life insurance savings market, pension funds suffer from a worse public value for money and trust perception. Only 45% of the EU population trust that benefits provided through pension funds will deliver good consumer and adequate retirement outcomes, compared to 50% in the case of insurance products.

This observation also holds true for both Greece and Cyprus, the comparative percentages are:

|

Trust in |

Trust in |

|

|

EU Average |

50% |

45% |

|

Greece |

54% |

46% |

|

Cyprus |

51% |

39% |

The fragmented nature of pension funds and lack of comparable data across the EU makes it more challenging to analyze the case for pension funds, but hopefully future Consumer Trend reports from EIOPA can fill in the gap for us.

Stephan Cronje

Partner and Founder of C.Y Actuaries

*The views expressed above are solely of the author and do not necessarily represent the view of Cronje & Yiannas Actuaries and Consultants Ltd.